As mining consolidates under pressure from the energy transition, the most resource-efficient companies are emerging as the industry’s likely winners.

By Alienor Hammer, Senior Environmental Research Analyst

As seen in Environmental Finance

A new wave of consolidation is sweeping through the mining industry. Multi-billion-dollar proposals, from Anglo American’s approach to Teck Resources to the mooted tie-up between Rio Tinto and Glencore, reflect a sector once again turning to dealmaking. At first glance, this may appear familiar. Mining has long moved in cycles, with mergers typically following commodity booms. However, this cycle looks different.

The current surge in M&A is being driven less by short-term price dynamics than by deeper structural forces. The energy transition is accelerating demand for critical minerals. At the same time, mineral deposits are becoming harder to exploit and environmental constraints are tightening. Together, these pressures are reshaping the economics of extraction and in turn, the logic of consolidation.

In this changing landscape, scale alone is no longer sufficient. Increasingly, the decisive factor is how efficiently resources can be produced.

A Structural Shift, Not a Cycle

Mining has always been cyclical. Periods of consolidation typically follow commodity upswings, as companies seek to expand production and reduce costs. But the current wave of M&A reflects more persistent pressures.

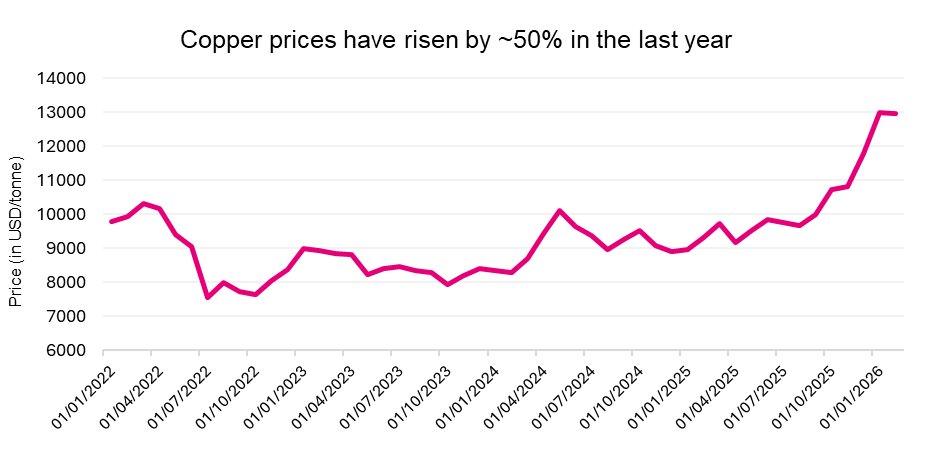

Demand for critical minerals (copper, lithium, nickel and rare earths) is rising rapidly as the global economy electrifies. Copper, in particular, is central to this transition, underpinning electric vehicles, renewable energy systems and power grids. This has driven a ~50% rise in copper prices in the last year, with major producers such as Freeport-McMoran and Antofagasta outperforming more diversified miners[1], and intensifying the race to secure long-term supply. Recent earnings calls reflect this shift: Lundin Mining, for instance, has highlighted a growing strategic focus on copper, supported by stronger revenues linked to higher prices[2].

Yet supply is slow to respond. Ore grades are declining, meaning more energy, water and capital are required to extract the same volume of material. The average copper ore grade has fallen significantly over time, contributing to a marked increase in the energy required to sustain production growth[1]. Studies show that the average copper ore grade in existing mines fell by 25% by 2016, from 2006[3]. Meanwhile, new mining projects are becoming slower and more expensive to develop, often requiring decades and substantial upfront investment before reaching production.

The result is a growing structural imbalance. Forecasts point to a sizeable copper supply shortfall within the next decade, with BloombergNEF estimating a 4.5 million tonne gap by 2027 and the IEA projecting a deficit of close to 10 million tonnes by 2040[4]. In such conditions, acquiring existing assets is often quicker, less risky and more economical than developing new ones. This is reflected in recent transactions: BHP and Lundin Mining, for example, formed a joint venture to consolidate control over the Filo del Sol and Josemaria copper projects[5], with the latter being at advanced-stage with relatively near-term production potential.

In this context, consolidation is first and foremost a strategic necessity.

The Rising Cost of Compliance

Alongside supply constraints sits a second, equally important force: environmental pressure.

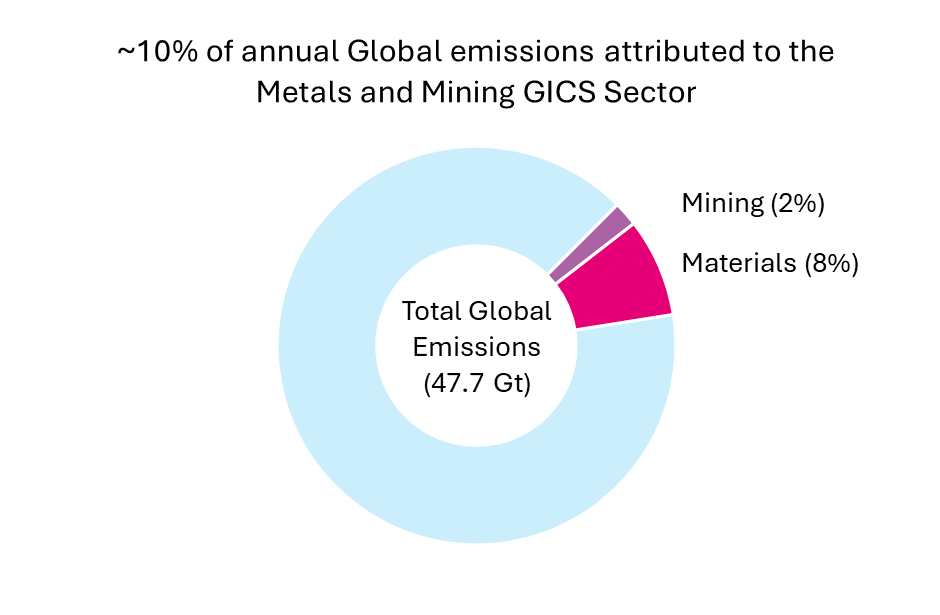

Mining remains a highly resource-intensive industry, with the metal and mining sectors accounting for roughly 10% of global emissions annually in 2024[6]. As regulatory scrutiny intensifies, the cost of compliance is rising. Carbon pricing, water scarcity and stricter waste standards are all adding to the baseline cost of production.

Companies are being pushed to invest in decarbonisation. Electrified fleets, renewable power integration and emerging technologies such as green hydrogen are gaining traction as solutions to operating models. These shifts are capital-intensive and tend to favour larger firms, not least because nearly 40% of emissions at mine sites come from diesel-powered machinery[3], making decarbonisation expensive and operationally complex.

Scale confers advantages: access to financing, the ability to absorb regulatory costs and greater flexibility in capital allocation. Smaller operators, by contrast, face increasing barriers to entry and expansion. This dynamic is reflected in rising deal activity in more regulated jurisdictions; in Canada, for example, natural resources M&A value rose sharply, contributing to a 133% increase in overall deal value to USD 178 billion in 2025[7]. The proposed Anglo American–Teck Resources combination, heavily weighted towards copper, is emblematic of this trend. It represents the biggest natural resources merger of the year, bringing together scale, long-life assets and exposure to transition metals. Following this merger, the resulting company will have a 70% exposure to copper and become one of the five largest copper producers in the world[8].

Environmental considerations, once peripheral, are now central to competitive positioning.

Why Efficiency Is Becoming the Deciding Factor

In this environment, not all production is equal.

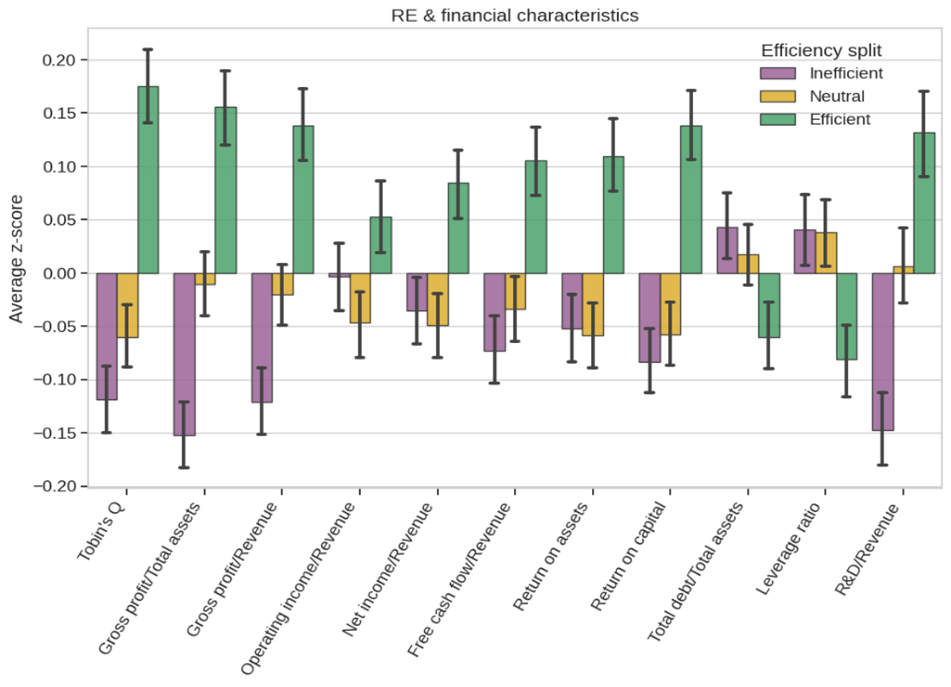

The key differentiator is no longer simply access to reserves, but the efficiency with which those reserves can be developed. Our research shows that companies that produce with lower emissions, reduced water usage and less waste are better positioned to manage rising costs and regulatory constraints. Resource efficiency, in this sense, is an economic consideration as well as an environmental one.

Osmosis research shows that more efficient companies tend to demonstrate stronger profitability, lower leverage and more stable cash flows over time. They are also better able to withstand external pressures, whether from commodity price volatility or tightening environmental standards.

Importantly, resource efficient companies are more likely to be consolidators rather than consolidation targets. Operational discipline and financial resilience provide the capacity to acquire assets and scale production. Less efficient operators, by contrast, face a narrower set of strategic options.

This pattern is increasingly visible across commodities. In copper, companies are prioritising long-life, high-quality assets that can be developed at lower environmental and economic cost. In lithium and rare earths, consolidation is focusing on integrating processing and refining capabilities, where efficiency gains are critical.

A New Lens for Investors

For investors, these developments carry important implications.

Traditional metrics (reserves, production volumes and cost curves) remain relevant, but are no longer sufficient. As environmental and operational constraints tighten, resource efficiency offers a more forward-looking indicator of performance. It reflects not only operational outcomes, but also management quality, capital discipline and the ability to adapt to structural change. In a sector undergoing transformation, these attributes are increasingly important.

The Bottom Line

Mining is becoming central to the energy transition. In the process, it is also becoming more complex and more capital-intensive. The current consolidation wave reflects a simple reality: mineral deposits are becoming harder to exploit, costs are rising and regulatory pressures are intensifying. The industry is adjusting accordingly. In this context, efficiency matters just as much as scale. And it is likely to be resource efficiency, not simply resource ownership, that determines which companies emerge as long-term winners.

Important Information

This document was prepared and issued by Osmosis Investment Research Solutions Limited (“OIRS”). OIRS is an affiliate of Osmosis Investment Management US LLC (regulated in the US by the SEC) and Osmosis Investment Management UK Limited (regulated in the UK by the FCA). OIRS and these affiliated companies (together, “Osmosis”) are wholly owned by Osmosis (Holdings) Limited, a UK-based financial services group. Osmosis has been operating its Model of Resource Efficiency since 2011.

The information contained in this document has been obtained by Osmosis from sources it believes to be reliable but which have not been independently verified. Information contained in this document may comprise an internal analysis performed by Osmosis and be based on the subjective views of, and various assumptions made by, Osmosis at the date of this document. Osmosis does not warrant the relevance or correctness of the views expressed by it or its assumptions. Except in the case of fraudulent misrepresentation or as otherwise provided by applicable law, neither Osmosis nor any of its officers, employments or agents shall be liable to any person for any direct, indirect or consequential loss arising from the use of this document.

This document does not constitute: a recommendation by, or advice from, Osmosis or any other person to a recipient of this document on the merits or otherwise of any companies mentioned in this document.

None of the company examples referred to above are intended as a recommendation to buy or sell securities. The information is intended only for the use of eligible and qualified clients and is not intended for retail clients.

The information does not constitute an offer or solicitation for the purchase or sale of any security, commodity or other investment product or investment agreement, or any other contract, agreement, or structure whatsoever. Recipients are responsible for making your own independent appraisal of and investigations into the products referred and not rely on any information as constituting investment advice. Investments like these are not suitable for most investors as they are speculative and involve a high degree risk, including risk of loss of capital. There is no assurance that any implied or stated objectives will be met. Osmosis has based the information obtained from sources it believes to be reliable, but which have not been independently verified. Osmosis is under no obligation and gives no undertaking to keep the information up to date. No representation or warranty, express or implied, is or will be made, and no responsibility or liability is or will be accepted by Osmosis, or by any of its officers, employees, or agents, in relation to the accuracy or completeness of the information. No current or prospective client should assume that future performance will be profitable the performance of a specific client’s account may vary substantially due to variances in fees, differing client investment objectives and/or risk tolerance and market fluctuations.

[1] The race for copper has brought a wave of mining mega-mergers

[3] Sustainability in metals and mining | Deloitte Insights

[6] ICMM – Global Mining and Metals Greenhouse Gas Emissions Dataset

[7] Canada Mining M&A Surge: Record Deals Drive Consolidation